Bumps in the Road

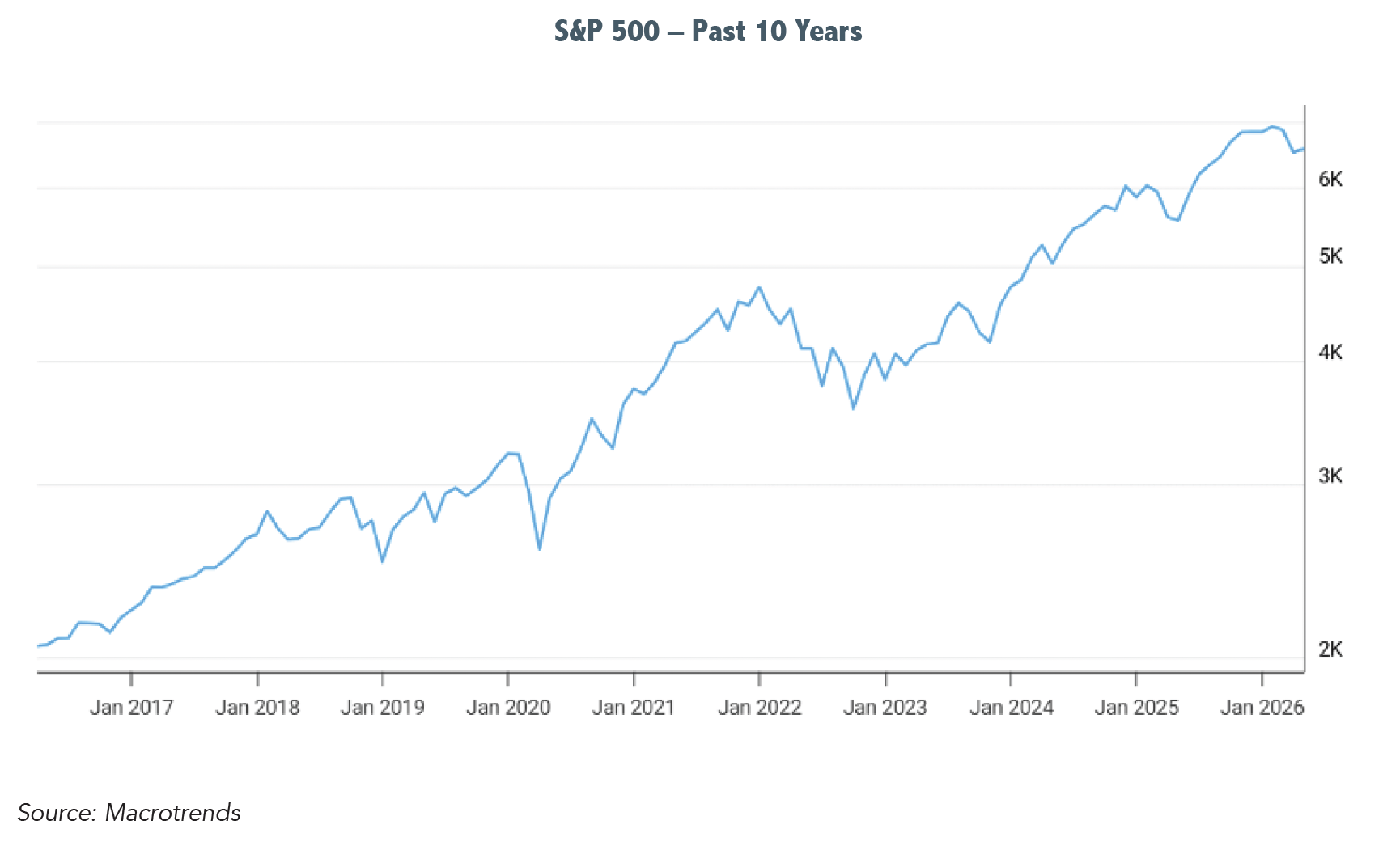

Broader equity markets (S&P 500, DJIA, NASDAQ) gave up ground in the first quarter of 2026, primarily due to concerns over AI-related valuations and geopolitical tensions from the war with Iran which began on 02/28/26. Companies trading at higher valuations declined the most as evidenced by the so-called Magnificent Seven (Apple, Alphabet, Amazon, Meta, Microsoft, Nvidia, and Tesla) which collectively fell over 10% during the quarter, compared with a 4.3% decline in the S&P 500. Energy companies soared along with the price of oil and gas.

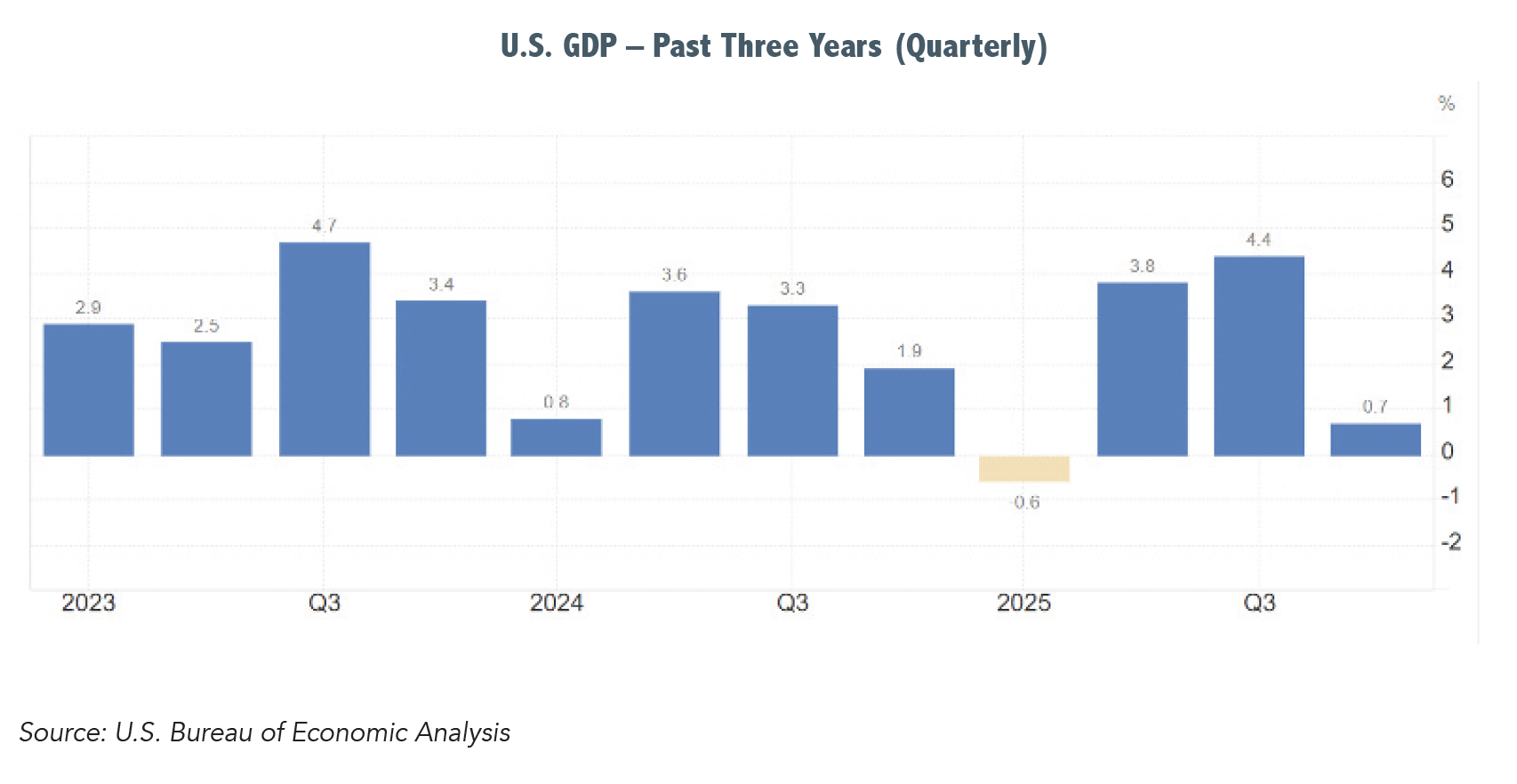

After years of stellar, narrow leadership by mega-cap technology stocks, Q1-26 marked a rotation in favor of value, small-cap and international equities. As broad U.S. indices pulled back, geopolitical conflict in the Middle East—specifically involving Iran—triggered a massive surge in energy and commodity prices, which became the quarter's standout performers. While the U.S. economy remained surprisingly resilient, expanding at a projected 2.0% to 2.6% rate, the quarter was marked by increased volatility, spurred by intensifying geopolitical conflict in the Middle East and sticky inflation.

The Federal Reserve paused its rate-cutting cycle in Q1-26, holding the Fed funds rate at 3.50%–3.75% as inflationary pressures from new tariffs and supply chain constraints proved more persistent than anticipated. Despite the challenging market environment, the probability of a near-term recession remained low, with AI-driven productivity gains and robust fiscal stimulus continuing to support corporate earnings. The economic narrative of Q1-26 shifted from a "soft landing" consensus to a "constructive growth" environment, though significant "K-shaped" divergences persisted, where top-income earners continued to thrive while middle- and lower-income consumers faced mounting affordability pressures.

The U.S. economy continues to display remarkable durability. While the fourth quarter of 2025 showed a dip in GDP growth (0.7% annualized) due to a government shutdown, the Atlanta Fed GDPNow index tracked Q1-26 growth at a healthier 2.0% to 3.0%. Early data in 2026 indicated that AI adoption began to move the "macro needle," driving a surprising surge in labor productivity—estimated near 3-4% annualized—which offset a tightening labor supply and restrained wage-driven inflation. Following several years of contraction, manufacturing showed signs of stabilization, with recent surveys pointing back toward expansionary territory.

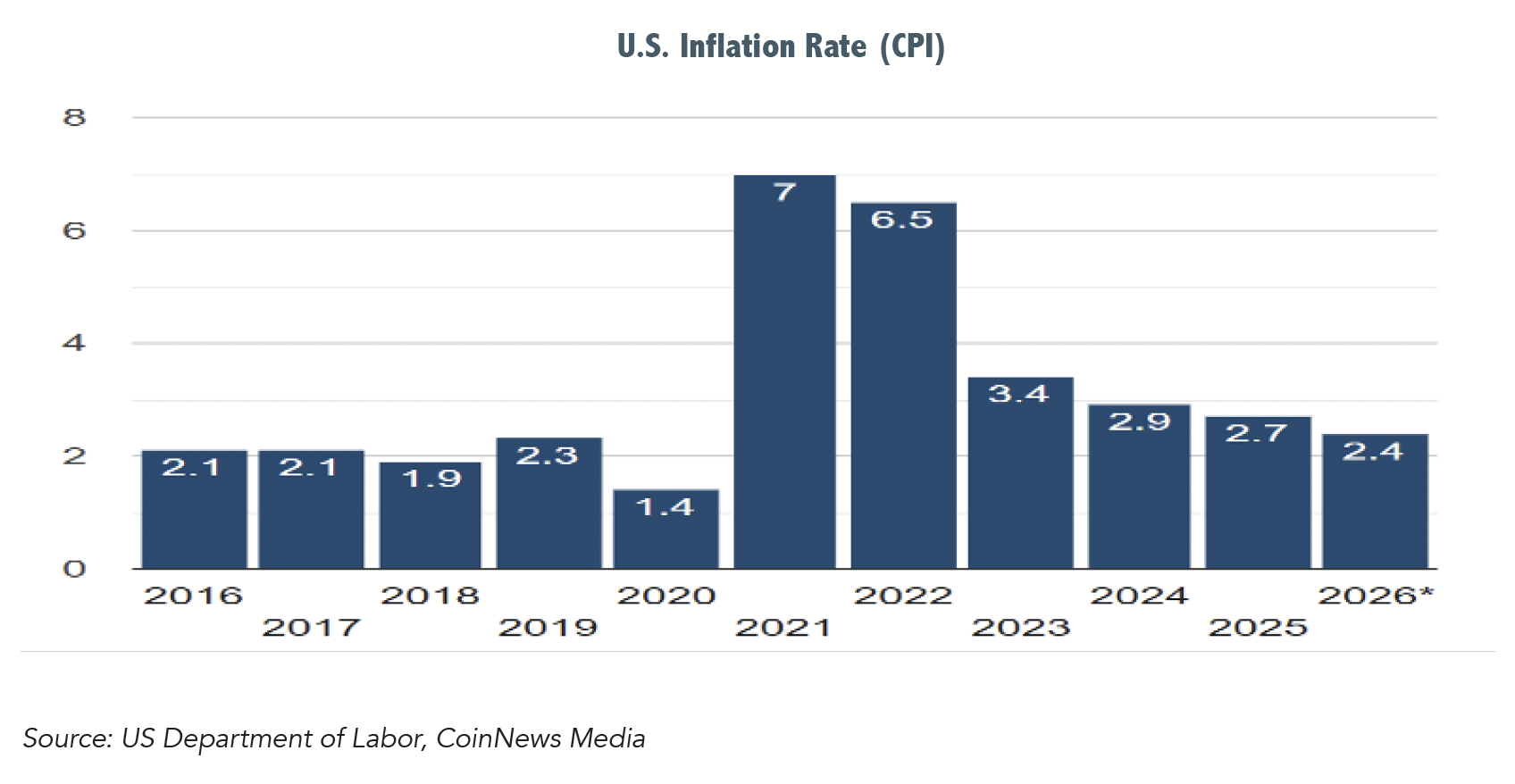

Headline inflation as measured by the CPI (Consumer Price Index) and PCE (Personal Consumption Expenditures Price Index) remained stubborn, hovering well above the Federal Reserve’s 2% target. The reintroduction of tariffs—after a brief legal disruption in February—maintained upward pressure on goods prices, as firms continued to pass increased costs through to consumers.

After the FOMC chose to leave rates unchanged in Q1-26, the market adjusted its expectations, moving from pricing in rapid rate cuts to expecting a "higher-for-longer" neutral rate. The labor market settled into a “Low-Hire, Low-Fire” stable, yet slowing, equilibrium. Unemployment hovered between 4.3% and 4.5%. Real consumer spending slowed but did not collapse, supported by rising real wages and a wealth effect from strong housing prices, though consumer confidence remained suppressed.

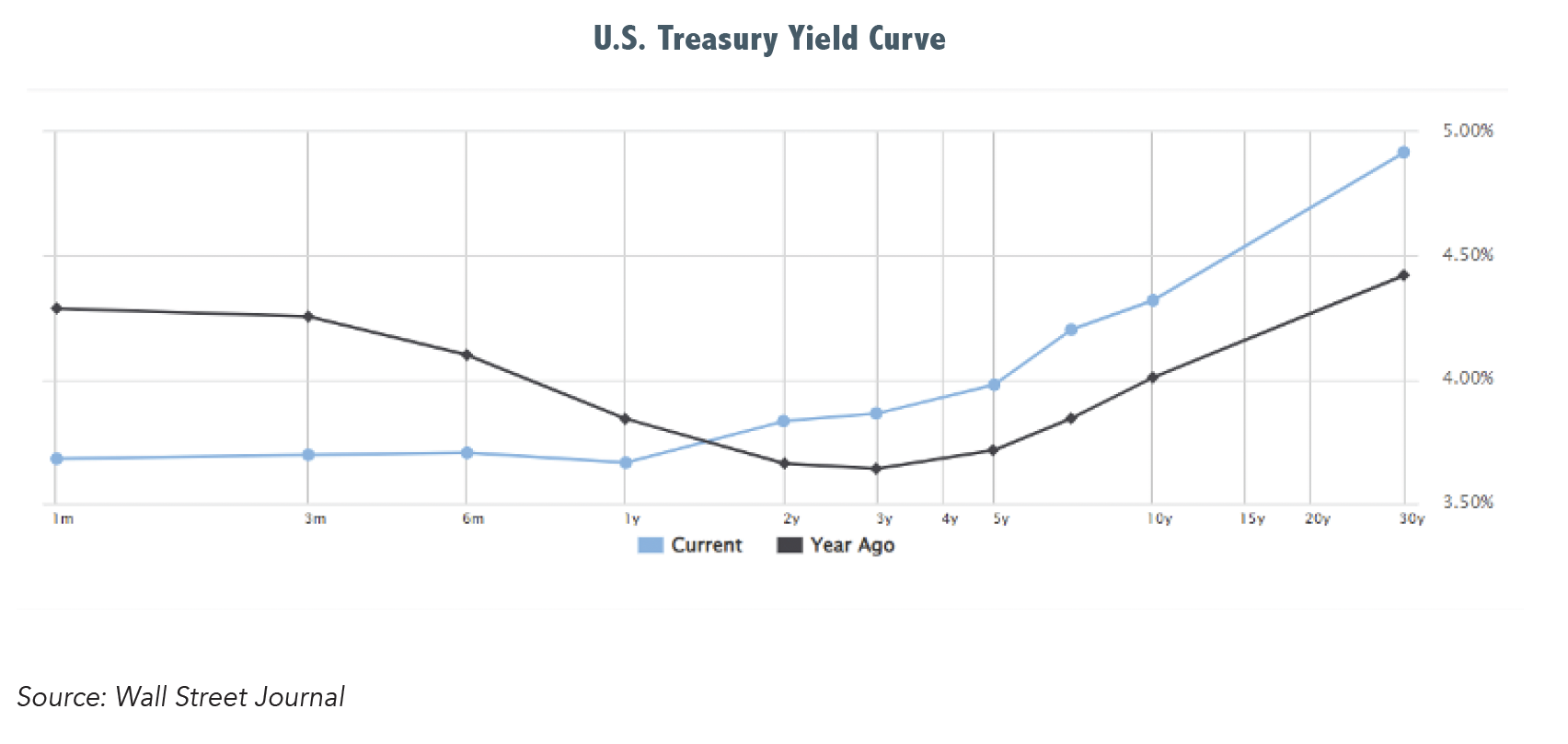

The first quarter of 2026 was a turbulent period for the bond market, characterized by an early rally on rate-cut optimism followed by a sharp selloff in March due to geopolitical tensions in the Middle East. The U.S. 10-year Treasury yield rose to 4.88% by quarter-end, erasing earlier gains, as inflation fears persisted. The 2-year/10-year yield curve continued to steepen, reaching its highest level since 2022, as investors demanded higher term premiums due to fears of rising U.S. debt and persistent inflation. Bonds provided limited total returns but fulfilled their role as income producers and portfolio stabilizers. Oil prices hit over $100 per barrel and gas at the pump breached $4 per gallon from the supply shock and closure of the Strait of Hormuz.

A prolonged war in the Middle East remains the primary downside risk, capable of triggering stagflation (low growth & high inflation). In addition, investors are critically reassessing whether the immense capital expenditure (CAPEX) on AI infrastructure will yield commensurate earnings in the short term, leading to "bubbly" valuations in certain mega-cap tech names. The Federal deficit continues to widen, projected at 5.8% of GDP in 2026, raising concerns over long-term fiscal sustainability. And finally, the approaching November midterm elections are likely to increase market volatility, as tariff, tax, and regulatory policies remain in flux. Despite the turbulent start to the year, the "expected case" for the remainder of 2026 remains constructive. If the Middle East conflict de-escalates, the Federal Reserve may deliver 1-2 rate cuts later in the year, providing a backstop for equities.

Investors should remember that there will always be bumps along their investment journey and market-moving events can rarely be predicted. Anyone betting on an assumed short-term outcome can quickly find themselves on the wrong side of that bet. The best defense is a good offense, and the best offense includes broad diversification, patience and an unemotional commitment to a plan. Of course, to be committed to a plan first means the existence of one. Without a formal financial plan and investment strategy, investors can succumb to a case of investor paralysis, or to impulsive temptations, running the risk of selling when they should be buying. Investors who have partnered with a team of dedicated, experienced financial advisors to create, implement and monitor that plan can rest knowing their work is done.

Ignore the bumps.