Against All Odds

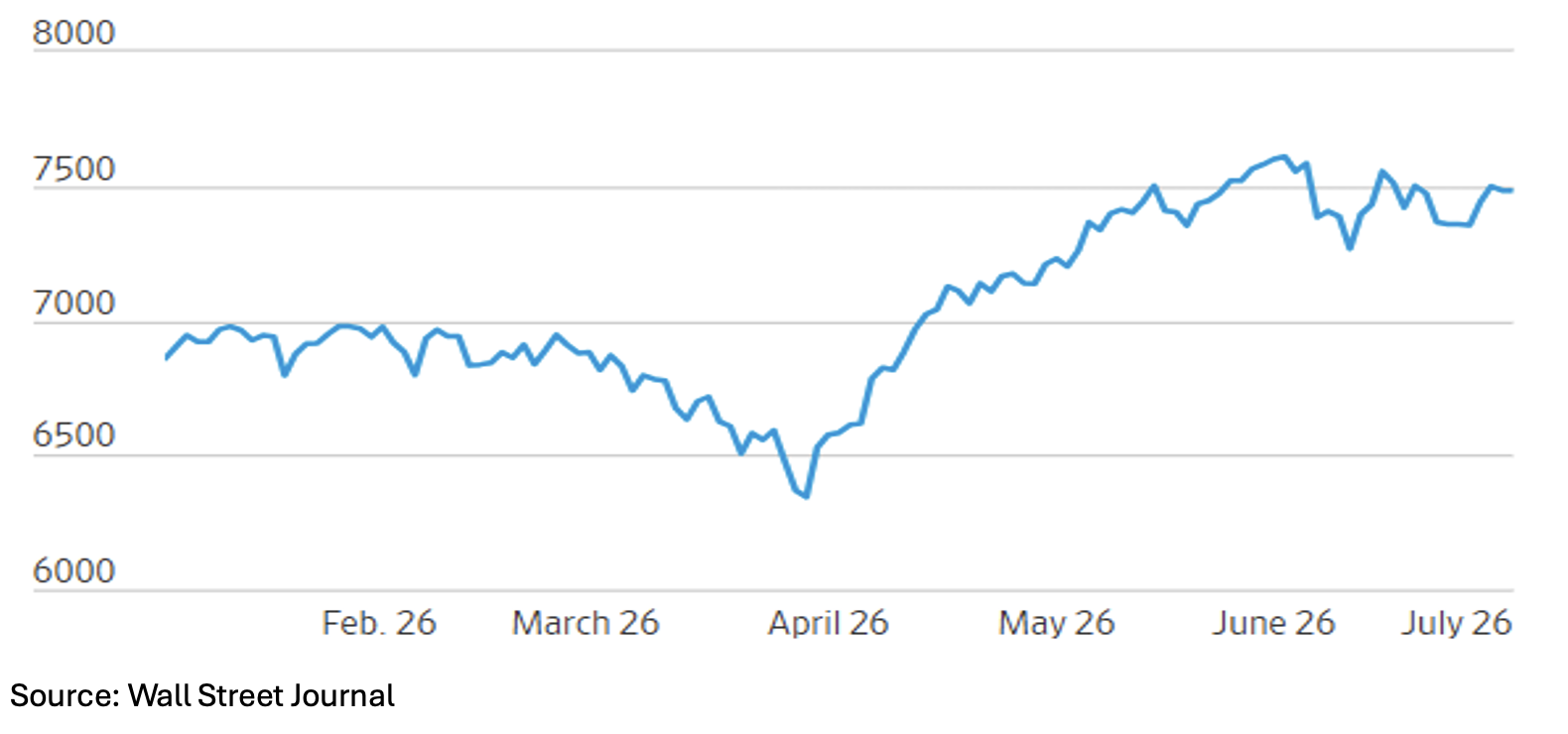

The second quarter of 2026 was characterized by more energy shocks from the war with Iran, an unexpected Federal Reserve pivot under newly confirmed Chairman Kevin Warsh, an AI-driven equity market rally that decoupled from underlying economic fundamentals, and an obsession with World Cup soccer. Against all odds, and despite concerns surrounding persistent inflation, geopolitical tension, and elevated interest rates, U.S. equities delivered one of the strongest second quarters in recent years. The benchmark S&P 500 soared an impressive 15.20% during Q2, driven by technology, software, and semiconductor companies.

S&P 500 (01/01/26 – 06/30/26)

The blockage of the Strait of Hormuz in early spring disrupted the disinflationary expectations that markets had priced in at the start of the year. A spike of over 40% in oil prices led forecasters to trim global GDP (Gross Domestic Production) growth estimates. Inflation metrics for 2026 were rapidly adjusted upward, pushing near-term headline CPI (Consumer Price Index) readings toward the 3.5% to 4% range. The Federal Reserve's preferred inflation gauge, Core PCE (Personal Consumption Expenditures), similarly saw its full-year 2026 projections bumped higher into the 3.3% to 3.5% threshold, well above the central bank's 2.0% mandate.

The economic and monetary response to this data was immediate. Newly confirmed Fed Chairman Kevin Warsh established a remarkably hawkish tone, refocusing the Fed entirely on its price-stability mandate. Warsh dismantled expectations for rate cuts that investors had held earlier in the year. Instead, the conversation transitioned toward holding interest rates elevated for a prolonged period, with an outside risk of a rate hike if headline inflation persistently breached 4.0% on a 12-month basis.

Following Chairman Warsh's pivot, the U.S. Treasury yield curve fluctuated, with the 10-year Treasury yield reacting to both inflation and “higher-for-longer” Fed messaging. The highly anticipated rate cuts that analysts had penciled in for late 2026 were pushed to late 2027, severely handicapping fixed-income returns relative to earlier expectations. Mortgage rates, which had briefly ticked down to 6.1% in Q1, rebounded above 6.5% in Q2, further constraining the housing market and holding back residential construction investment.

10-Year U.S. Treasury Note

Following historic rallies over the previous year, precious metals and cryptocurrencies encountered a severe bout of profit-taking and technical liquidation. Gold suffered its largest single-month decline since 1975, and silver crashed more than 50% from its recent highs. Historically, such assets act as inflation hedges or safe-havens in times of war and geopolitical crises. However, in Q2 2026, gold, alongside Bitcoin, registered as two of the worst-performing major global asset classes.

U.S. real GDP grew at an annualized rate of 2.0% in the first quarter, driven by solid consumer spending and massive capex (capital expenditures). However, Q2 GDP forecasts were consistently trimmed downward to a range of 2.0% to 2.4%. The economy experienced a stark divide between corporate technology investment and consumer health. AI related capex showed no signs of slowing, with hundreds of billions poured into data centers, cloud infrastructure, and hardware.

Conversely, the American consumer—who accounts for 65% to 70% of U.S. GDP, faced significant headwinds. Despite near-full employment, labor market anxiety increased due to a "low-hire, low-fire" environment and the looming threat of AI-driven job displacement. Average national gas prices flirted with $4.00, sapping discretionary spending power. Concurrently, negative real wage growth, diminishing savings, and elevated tariff impacts led to some of the lowest consumer confidence readings recorded by the University of Michigan in recent years.

This dynamic showcased the market's intense focus on AI productivity. Rather than relying on widespread job creation or broad-based consumer retail strength, the stock market rally was supported by robust corporate earnings that repeatedly exceeded analyst estimates. The AI revolution allowed major tech corporations to project continued double-digit earnings growth for the remainder of 2026. However, this concentration also meant that a large drag on the broader index came from investors rotating out of older, legacy mega-caps and value stocks that were hobbled by rising interest rates and input costs.

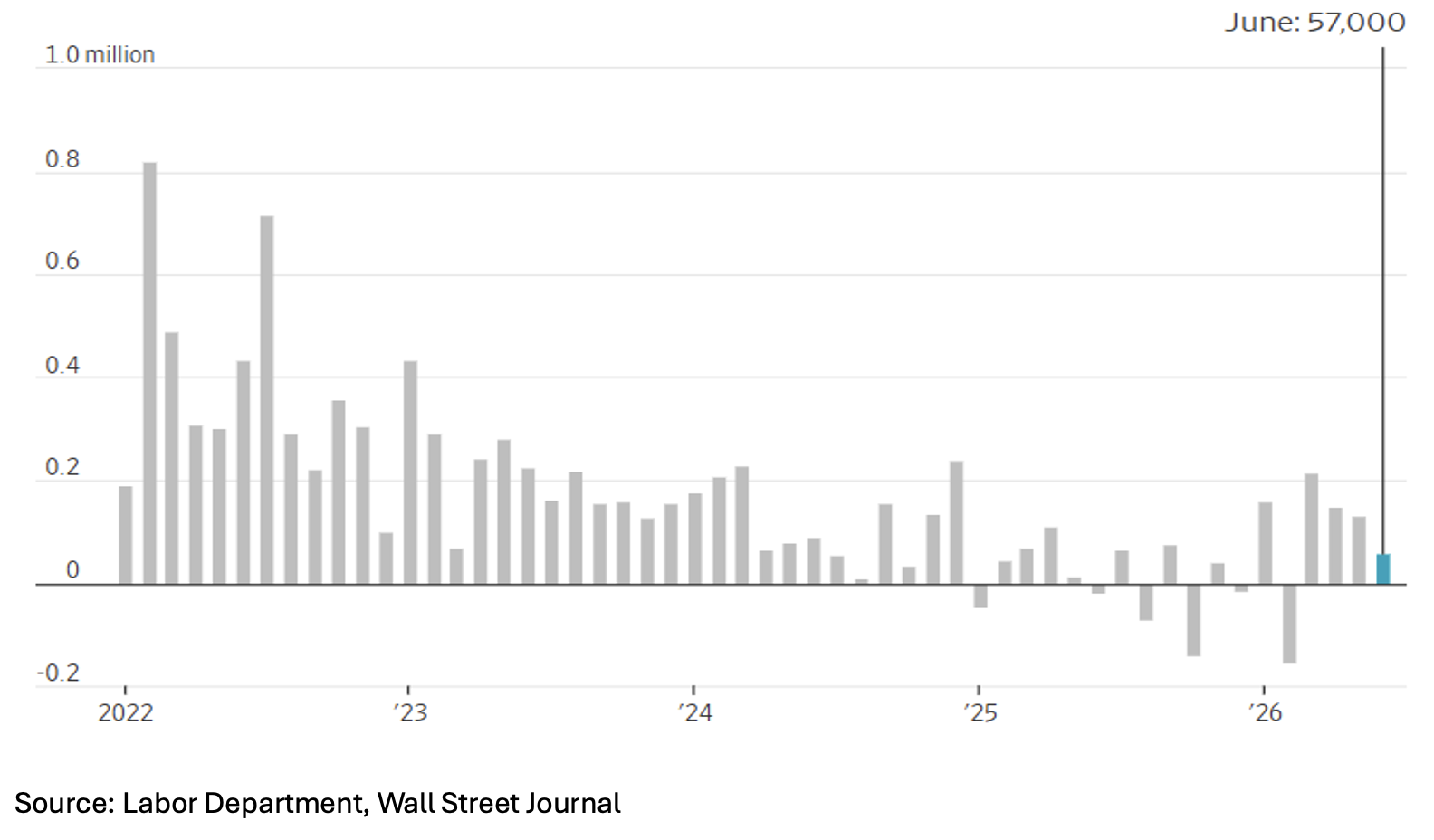

Nonfarm Payrolls, Change from a Month Earlier

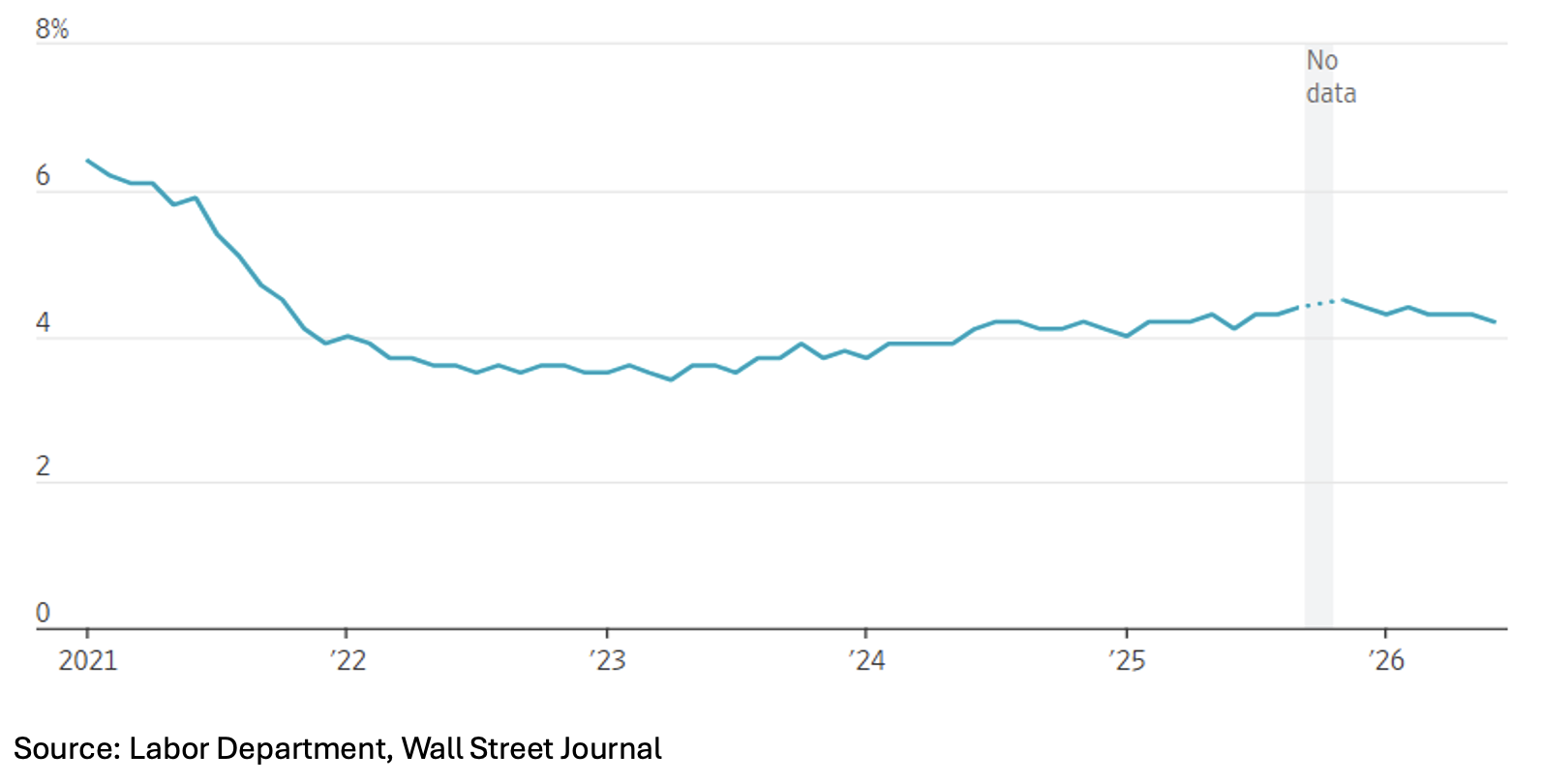

In Q2 2026, the U.S. labor market cooled significantly. Job creation missed expectations and hiring plans slowed. The labor market added just 57,000 jobs in June, following a brief bump earlier in the quarter. Downward revisions revealed the spring was much weaker than originally reported. Data for April and May were revised downward by a combined 74,000 jobs. The unemployment rate dropped to 4.2% in June, though economists attribute this decline largely to workers dropping out of the labor force rather than a surge in new hiring. Still, the job market appears to be on firmer footing than it was in the second part of last year. The economy added an average of 92,000 jobs per month over the first half of this year. In the final six months of last year it shed 8,000 jobs each month, on average.

Halfway through 2026, the U.S. economy is continuing to hum thanks to solid consumer spending and strong business investment in AI. Hiring has stabilized in recent months after a weak patch during the fall and winter. Even so, inflation has picked up because of the conflict in Iran. That has eaten into wage gains and weighed on consumer sentiment. Measures of consumer confidence rose slightly in June on lower gasoline prices, but households continue to feel stressed about the cost of living and the labor market. The Conference Board said recently that the percentage of consumers saying jobs were “hard to get” rose to the highest-level last month since January 2021. Gasoline prices, which spiked after the start of the Iran war, have eased in recent weeks, although they remain above their year-ago levels.

Unemployment Rate

As the Federal Reserve charts a new, hawkish course under Kevin Warsh, the financial markets are left navigating a highly complex environment characterized by high stock valuations, vulnerable fixed-income positioning, and immense global geopolitical uncertainty.

Stay focused, follow your plan, consult with your team of financial advisors, and enjoy rooting for your favorite FIFA World Cup team.